Mutual funds are one of the most popular investment choices in India today—but many investors often overlook a crucial detail: whether to invest through a regular plan or a direct plan.

This decision may seem minor on the surface, but over the years, it could impact your returns more than you’d expect.

It all starts with something called the expense ratio.

Why the Expense Ratio Matters More than You Think

Every mutual fund comes with a cost—called the expense ratio. It’s a small percentage deducted annually from your invested amount to cover the fund’s operational costs. Think fund manager fees, marketing expenses, distributor commissions, etc.

While it might look like a small number (say 1.5% or 0.8%), when you’re investing lakhs over 10–15 years, the impact becomes substantial.

And here’s where things get interesting. The expense ratio is higher in regular mutual funds because it includes distributor commissions. Direct mutual funds, on the other hand, eliminate this middle layer and pass the savings directly to you.

So naturally, that leads us to the question—what are these two plans, and how do they actually differ?

But first let’s understand what regular and direct mutual funds really mean.

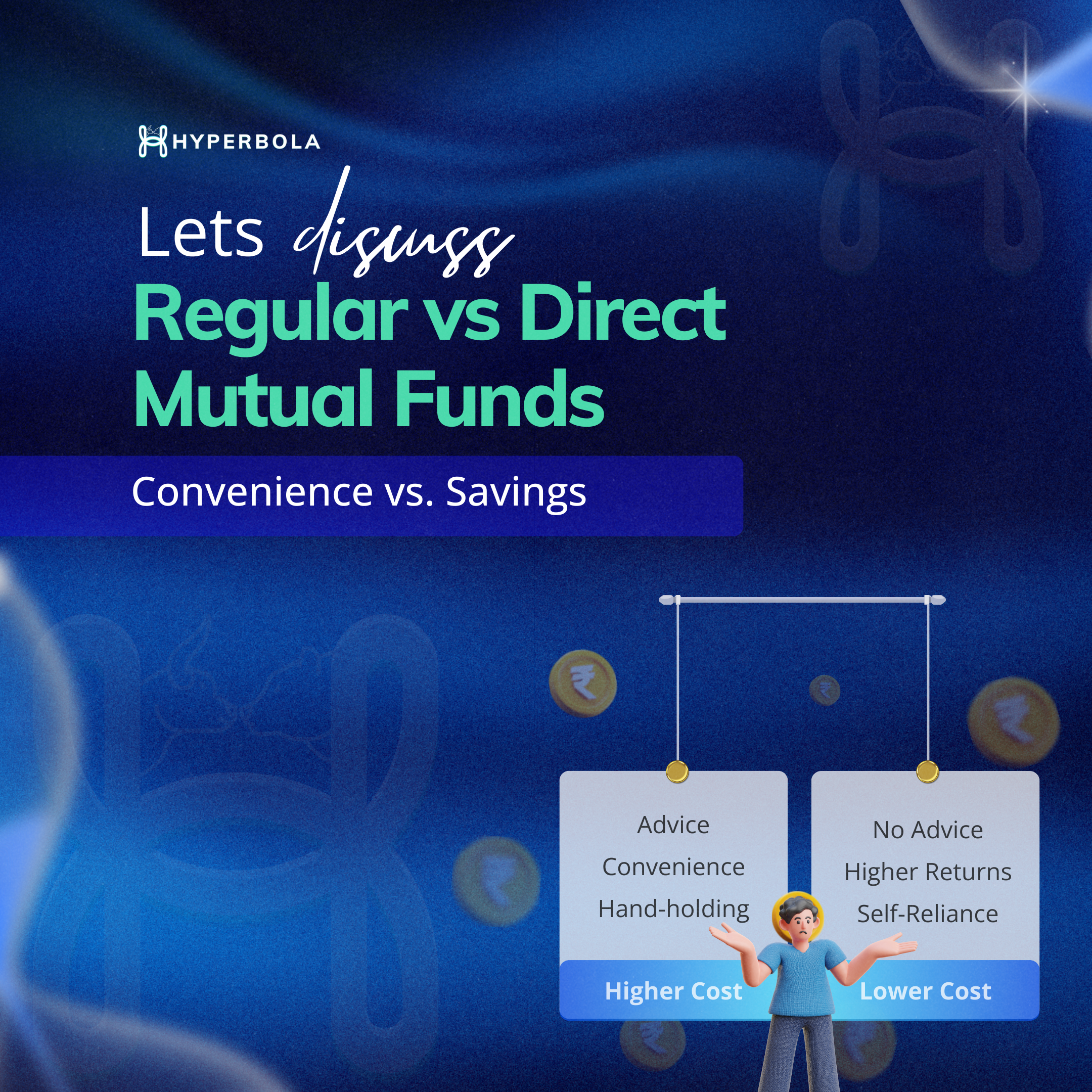

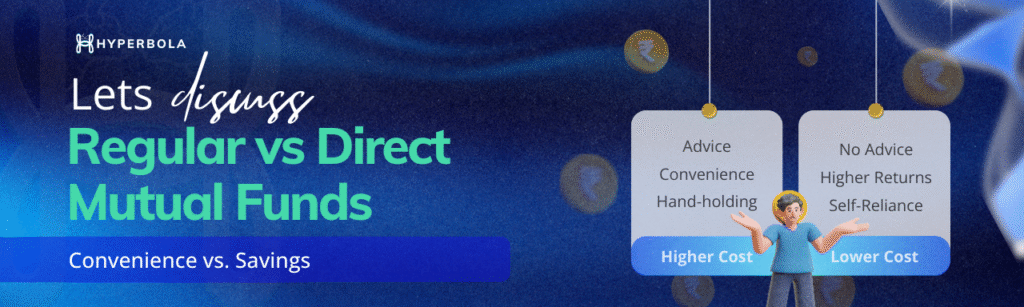

What Are Regular and Direct Mutual Funds?

Regular and Direct Mutual Funds are not different schemes—they’re two different ways to invest in the same mutual fund, but with different cost structures and investor experiences.

Let’s break them down.

What is a Regular Mutual Fund?

A regular mutual fund is the more traditional route—one where you invest with the help of an intermediary like a bank, financial advisor, or brokerage platform. These intermediaries act as a bridge between you and the fund house.

They recommend funds, assist with onboarding, and may even help manage your investments over time.

However, this convenience comes at a cost. Fund houses pay these distributors a commission—taken from your investment returns via a higher expense ratio.

So while you’re not directly writing them a cheque, you are paying for the service by earning slightly lower returns over time.

If you’re someone who prefers guidance, or if you’re just starting out and don’t mind paying a little extra for hand holding, regular mutual funds can offer peace of mind.

What is a Direct Mutual Fund?

A direct mutual fund, as the name suggests, cuts out the middleman.

Here, you invest directly through the mutual fund house’s website, mobile app, or a zero-commission platform like Coin, Paytm Money, or Groww. No advisors. No commissions. No extra charges.

This means the expense ratio is lower, and you get better long-term returns. For instance, over a period of 10–15 years, even a 1% difference in expense ratio can result in lakhs of rupees more in your portfolio.

But there’s a trade-off: you’re on your own. You need to pick the right fund, track your performance, and make decisions like switching or rebalancing. If you’re comfortable doing that—or willing to learn—direct plans can be a powerful, cost-effective option.

Key Differences Between Regular vs Direct Mutual Funds

Now that we’ve set the base, let’s compare these two plans in detail to understand their practical implications.

1. Mode of Investment

In a regular fund, you invest via intermediaries—distributors, advisors, or banks. In a direct fund, you go straight to the source—the AMC’s portal or approved direct platforms.

This affects how much guidance you get during the investment process. With regular plans, you typically receive assistance in choosing and maintaining your portfolio.

2. Expense Ratio

This is a big one. Regular mutual funds have a higher expense ratio due to embedded commissions. Direct mutual funds cut out this layer, offering a lower expense ratio and better long-term compounding.

Over time, this difference can translate into lakhs in extra returns for the same mutual fund.

3. Returns

Because of the lower expenses, direct mutual funds almost always yield higher returns than their regular counterparts—everything else being equal.

This doesn’t mean one fund performs better than the other; it’s just that direct plans shave off fewer charges from your gains.

4. Guidance and Handholding

In regular plans, you get access to professional guidance, fund selection help, and sometimes even periodic portfolio reviews. Direct plans require you to do your own research or use tools/platforms that simplify the process.

How to Identify a Regular or Direct Mutual Fund.

Now that you know the theoretical difference between regular vs direct mutual funds, here’s how to check which one you’ve actually invested in.

It’s easy to assume you’re investing in the lower-cost option—until the numbers tell a different story. Here’s how you can find out:

1. Check the Fund Name Carefully

The easiest way to identify your plan is to look at the name of your mutual fund scheme.

- If the name contains the word “Direct” (like HDFC Flexi Cap Fund – Direct Plan – Growth), it’s a direct mutual fund.

- If it says “Regular” or doesn’t mention “Direct” at all, it’s a regular fund.

This label is clearly visible on your investment statement or the platform you used to invest.

2. View Your Mutual Fund Statement or CAS

Every mutual fund investor receives a CAS (Consolidated Account Statement) from NSDL or CDSL. It lists all your mutual fund holdings across AMCs.

- Check the column that mentions “Plan Type” or look for the word “Direct” in the scheme name.

- If it’s missing, it’s most likely a regular plan.

This is the most foolproof method if you’re unsure where you invested from.

3. Log Into CAMS or KFintech

CAMS and KFintech are registrar platforms for mutual funds in India. By logging in with your PAN and email/phone, you can see all your investments across different AMCs.

- These platforms clearly label plans as Direct or Regular.

- Some even provide an option to switch from regular to direct if you wish.

This is especially useful if you invested through multiple platforms.

4. Use Your Investment Platform’s Dashboard

If you’re using apps like Zerodha Coin, Groww, Paytm Money, or AMC websites, check your portfolio section.

- Direct investment platforms will always show Direct plans.

- If you used a bank, relationship manager, or distributor, chances are you’ve been put in a Regular plan by default.

A quick dashboard check can reveal what you’re really paying for.

Peace of Mind: Using a Regular vs Direct Mutual Funds Calculator.

Choosing between regular vs direct mutual funds doesn’t have to be confusing. That’s where a regular vs direct mutual funds calculator comes in handy.

What is it?

It’s a simple online tool where you enter your investment amount, tenure, and fund details. It shows you the projected returns for both direct and regular plans.

How to Use It?

Just go to any credible investment platform or AMC website, find the calculator tool, and:

- Enter your monthly SIP or lump sum amount

- Choose your expected return rate

- Select the investment duration

In seconds, it shows the difference in returns between the two options. The results can be eye-opening—sometimes a difference of lakhs for long-term investors.

Why it Helps.

This calculator removes guesswork. It gives you clarity on how much you’re paying in fees and how much you’re losing in potential gains over time.

Which is Better: Direct or Regular Mutual Fund?

Now let’s break down the question: Which is better—direct or regular mutual fund?

While the numbers may seem to favour one, the right choice really depends on who you are as an investor and how much guidance you need on your financial journey.

1. Choose Regular Mutual Funds if You Need Guidance

If you’re new to mutual funds, unsure about fund selection, or want periodic advice, regular plans offer personalised service and peace of mind. You get access to a trusted advisor or distributor who understands your goals, helps choose the right funds, monitors performance, and recommends timely portfolio adjustments.

For investors who don’t have the time—or the interest—to decode market reports or track fund ratings, this handholding makes a big difference.

You can focus on your life or business while your investments are being looked after by someone who does this for a living.

Yes, you’ll be paying a slightly higher expense ratio for this convenience. But think of it not just as a cost—but an investment in expert guidance and emotional confidence. Most people don’t fully understand the investment landscape, and that’s completely normal.

In that case, paying for peace of mind is often the smartest financial decision you can make.

2. Choose Direct Mutual Funds if You’re Comfortable with Self-Management

If you’re financially confident, enjoy doing your own research, and are comfortable managing your money without external support, direct plans can help you maximize returns.

You skip the distributor commission, potentially saving 0.5%–1.2% in expense ratio every year. For long-term investors, this can translate into lakhs of extra gains—especially in large portfolios or retirement-focused investments.

Direct plans also give you full control and transparency, which is ideal for those who like to be hands-on with their wealth-building strategy.

But it does require time, discipline, and a good understanding of the markets.

So, What’s the Verdict?

While both options have their merits, the more practical and stress-free route for most investors is the regular mutual fund.

You get expert help, save time, and avoid the guesswork that comes with DIY investing.

If your goal is not just to save costs, but to make smart, confident, and goal-aligned decisions—regular plans are the better choice. Especially when you’re backed by a platform that simplifies your investment journey, while keeping you informed every step of the way.

Still wondering how it all adds up?

Let’s break down the key advantages and disadvantages of direct and regular mutual funds so you can compare them side-by-side.

Advantages and Disadvantages.

Both regular vs direct mutual funds come with their own set of strengths and trade-offs.

But when you’re looking beyond just numbers—into confidence, consistency, and peace of mind—regular plans often offer more value than they’re credited for.

Regular Mutual Funds

Pros:

- Professional advice and goal-based planning

You’re not just picking a fund; you’re investing with expert guidance tailored to your goals, time horizon, and risk appetite. - Ideal for first-time or busy investors

Whether you’re starting out or don’t have time to track the market, regular plans offer a smoother, more confident investing experience. - Emotional support during market ups and downs

In volatile markets, having a human advisor to guide you can prevent panic-driven decisions—a major factor in long-term success.

Cons:

- Higher expense ratio

Yes, regular plans charge slightly more, but that’s the cost of access to personalised support. - Slightly lower returns vs direct plans

Over the long term, commissions can add up—but the value of consistent, guided investing often outweighs marginal differences in returns.

Direct Mutual Funds

Pros:

- Lower cost structure = higher potential returns

Since there’s no distributor involved, you save on commissions—which can lead to higher returns, especially over decades. - Full control of investment decisions

For seasoned investors who enjoy autonomy, this freedom is a big plus. - Transparent, online-first approach

Everything is available at your fingertips if you know where (and how) to look.

Cons:

- Requires financial literacy and time

You’ll need to understand risk, performance metrics, asset allocation, and market trends—or risk making uninformed choices. - No support if you’re stuck or confused

There’s no advisor on standby. You’re fully responsible for your decisions—good or bad.

Conclusion.

Both plans have their place, depending on your needs and comfort level. But if we purely go by numbers and long-term wealth creation, direct mutual funds have a clear edge. Lower expenses, higher returns, and full transparency make them ideal for today’s digital-savvy investor.

That said, if you value expert advice and don’t mind paying a bit extra for convenience, regular mutual funds are still a solid choice.

However, always seek professional advice before deciding the best for yourself. Hyperbola is an AMFI-regulated Mutual Fund Distributor, assisting its investors in making risk profile–based decisions.

Sign up on Hyperbola to better assess your risk profile and start investing in Mutual Funds.