In today’s investment world, choices are plenty—but clarity is rare.

You may have heard terms like ETFs and Mutual Funds tossed around during a financial planning session or on a market news channel. They both sound familiar, promise growth, and offer diversification. But how do they actually differ? And more importantly, which is better for your long-term goals?

Let’s clear the fog and walk through the essentials of ETF vs mutual fund—not just definitions, but how each works, how they’re taxed, traded, and tailored for different kinds of investors.

Why the ETF vs Mutual Fund debate matters.

With the rise of passive investing and more people looking for cost-effective and diversified options, investors are increasingly choosing between exchange traded funds vs mutual funds.

While mutual funds have been around longer and are more traditional, ETFs are gaining ground rapidly in India due to their flexibility, low cost, and real-time trading capability.

As more investors look beyond fixed deposits and insurance to build wealth, understanding the mutual fund vs ETF debate is no longer optional. It’s essential.

What Are ETFs and Mutual Funds?

Both mutual funds and ETFs (Exchange Traded Funds) are pooled investment vehicles.

That means your money is combined with other investors’ money to buy a basket of securities like stocks, bonds, or commodities.

They help you diversify your investment without having to buy each security individually.

But while they sound similar on the surface, the way they function underneath is quite different—and that’s where your investment choices become interesting.

ETF vs Mutual Fund: Breaking down the key differences

Both ETFs and mutual funds aim to help you diversify your investments. But how they get you there — and how you experience that journey — can be quite different.

Let’s break down the differences in a way that helps you choose what fits you better.

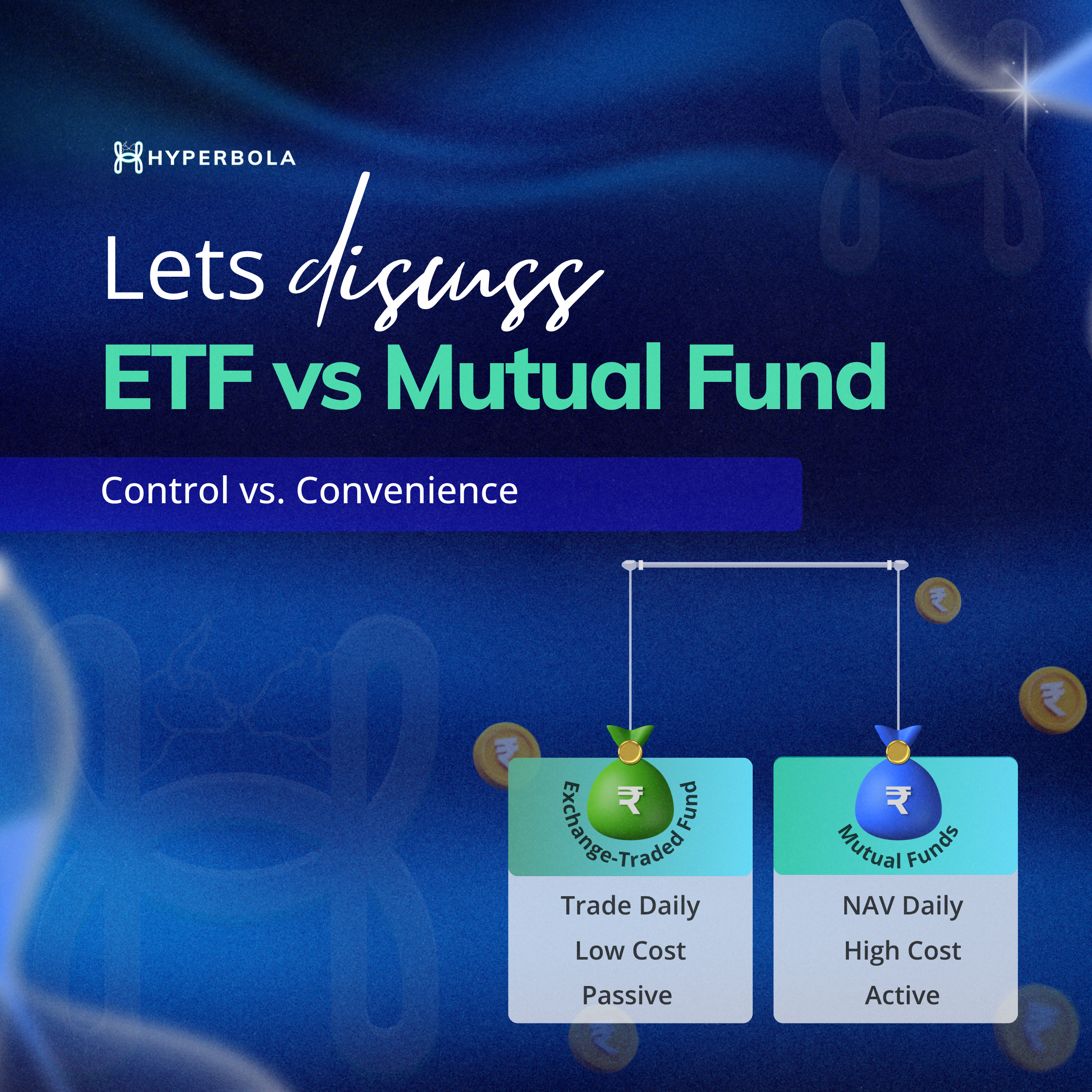

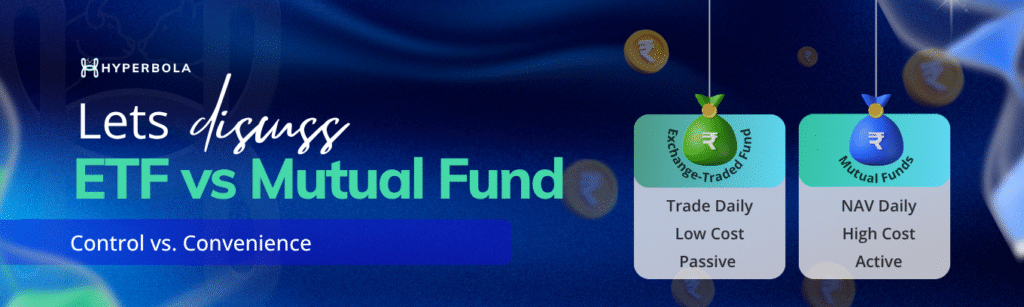

1. Trading Style and Accessibility

ETFs are traded on the stock exchange like regular shares, which means you can buy or sell them anytime during market hours. This gives them flexibility and transparency in pricing.

Mutual funds, on the other hand, are bought or redeemed directly from the fund house at the day’s NAV (Net Asset Value). While this means you can’t “trade” them during the day, it removes the pressure of market timing — a benefit for long-term, hands-off investors who prefer to stay focused on their goals.

2. Costs and Charges

ETFs usually have lower expense ratios because most are passively managed. You don’t pay for active fund management or research. However, you do pay brokerage and transaction costs every time you buy or sell an ETF.

Mutual funds might have slightly higher fees, especially actively managed ones. But those fees go toward expert fund management, continuous research, and in some cases, better returns than market benchmarks. Also, with direct mutual funds, you can significantly cut down on distribution costs.

3. Tax Efficiency

ETFs are generally more tax-efficient because of how they’re structured — especially in international markets where in-kind transfers reduce capital gains. In India, however, the tax treatment for ETFs and mutual funds is largely the same when they fall under the same asset class (like equity or debt).

That said, mutual funds offer Systematic Withdrawal Plans (SWPs), which can be a more tax-efficient way to create regular income, especially post-retirement — something ETFs don’t currently offer as seamlessly.

4. Management Style

Most ETFs are passively managed — they aim to mirror an index like the Nifty 50 or Sensex. This means lower costs and predictable returns, but they’ll never “beat the market.”

Mutual funds come in both active and passive flavours. Actively managed mutual funds aim to outperform the market through research and fund manager insights. If you believe in professional expertise and are looking to beat the average, mutual funds might give you that edge.

5. Investment Discipline and Automation

Mutual funds support Systematic Investment Plans (SIPs), which help you build a habit of investing monthly without having to time the market. This automated, rupee-cost averaging approach is a major psychological and financial advantage.

While ETFs offer flexibility, they don’t support SIPs through all platforms, and require manual investing via a Demat account. This suits investors who are comfortable taking a more active role.

Similarities between ETFs and Mutual Funds: More in Common than you think

Though they differ in structure, ETFs and mutual funds share common goals: diversification, professional management, and access to a variety of asset classes.

1. Diversification

Both instruments pool investor money to buy a wide range of securities. Whether it’s a Nifty 50 ETF or a large-cap mutual fund, you’re getting exposure to multiple companies, which reduces the risk compared to investing in individual stocks.

2. Regulated by SEBI

In India, both ETFs and mutual funds are regulated by SEBI (Securities and Exchange Board of India), which means there are strict guidelines on transparency, disclosure, and investor protection.

3. Access to Varied Asset Classes

Both offer access to equities, debt, gold, international markets, and even hybrid strategies. Whether you’re conservative or aggressive, there’s a product that fits your risk profile in either format.

Types of ETFs and Mutual Funds – Know your options

Now that we’ve understood the mutual fund vs ETF basics, let’s dive into the different types available for each.

Types of Mutual Funds

Mutual funds in India are classified based on their investment objective:

- Equity Mutual Funds: Invest primarily in stocks and aim for long-term growth.

- Debt Mutual Funds: Invest in bonds, government securities, and fixed-income instruments.

- Hybrid Funds: Combine equity and debt to balance risk and return.

- Index Funds: Passive mutual funds that mirror an index like Nifty or Sensex.

Example: A young investor might start with a SIP in a hybrid fund to get balanced exposure to both equity and debt.

Types of ETFs

ETFs are generally classified based on what they track:

- Index ETFs: Track market indices like Nifty 50, Sensex.

- Sector ETFs: Focus on a specific sector like banking, IT, or pharma.

- Gold ETFs: Invest in physical gold and trade like any stock.

- International ETFs: Provide exposure to foreign markets like the Nasdaq or S&P 500.

Example: An investor who wants to hedge against currency depreciation might invest in a US-based ETF that tracks the S&P 500.

Which Is Better for You: Mutual Fund or ETF?

Choosing between mutual fund or ETF— which is better depends on your goals, risk appetite, and comfort with market tools.

When Mutual Funds might work Better.

- If you’re looking for a set-it-and-forget-it investment experience.

Mutual funds support Systematic Investment Plans (SIPs), which automate your monthly investments. This not only builds financial discipline but also takes the emotional guesswork out of market timing — perfect for long-term wealth building. - If you’re comfortable delegating investment decisions to professional fund managers.

With mutual funds, you get access to expert fund managers who actively track the markets, rebalance portfolios, and identify growth opportunities. This can result in better risk-adjusted returns, especially in uncertain or complex economic conditions. - If you prefer paperless investing without the need for a Demat account.

Mutual funds can be purchased directly online through platforms or apps — no Demat account needed. This makes them far more accessible and beginner-friendly, especially for those who want a smoother entry into investing without the technical overhead.

When ETFs might work Better.

- If you want real-time trading flexibility like stocks.

ETFs are traded on stock exchanges, so you can buy or sell them anytime during market hours at live prices. This is ideal for investors who want more control over timing and execution, especially in fast-moving markets. - If you’re looking for a low-cost investment option.

Most ETFs are passively managed and mirror an index, so the expense ratios are generally lower. That means more of your money stays invested — which can have a big compounding impact over the long term. - If you’re already using a Demat account and are comfortable placing trades.

ETFs work seamlessly for investors who are familiar with equity markets and already have a brokerage or Demat account. If you’re used to buying and selling stocks, ETFs might feel like a natural extension of your investment strategy.

In general, mutual funds are ideal for long-term, hands-off investors, while ETFs may suit cost-conscious, self-directed investors who like a bit more control.

Are ETFs Riskier Than Mutual Funds?

When it comes to ETF vs mutual fund, many investors wonder which one carries more risk.

While both invest in similar assets like stocks or bonds, the way they’re structured and traded can make ETFs feel riskier—even if the underlying investments are alike.

Real-Time Volatility and Perception of Risk.

ETFs trade on the stock exchange and their prices fluctuate all day, just like individual shares. This real-time pricing can trigger emotional reactions, especially during volatile markets. In contrast, mutual funds are priced just once a day at their NAV, offering a calmer, more passive experience.

So, while the actual investment risk may be the same, ETFs often appear more volatile—purely because you’re watching prices move live.

Liquidity and Trading Complexity.

Another factor is liquidity risk. Popular ETFs generally trade smoothly, but lesser-known or thematic ETFs may have fewer buyers and sellers, leading to price deviations from their NAV due to wider bid-ask spreads. Mutual funds, however, are bought and sold directly from the fund house at NAV—making pricing more predictable.

Behavior and Control.

Because ETFs require active monitoring and a Demat account, they demand more from you as an investor. This can increase the chances of emotional decisions—buying high or selling low. Mutual funds, especially through SIPs, promote discipline and reduce the urge to time the market.

Bottom Line

So, are ETFs riskier than mutual funds?

Not inherently. The core risk depends on what you’re investing in, not the wrapper.

But the experience of risk—due to price visibility, trading dynamics, and investor behavior—can feel more intense with ETFs.

If you prefer low-touch, long-term investing, mutual funds may suit you better. If you’re market-savvy and value flexibility, ETFs offer a powerful, cost-effective option.

Conclusion

At the end of the day, both ETFs and mutual funds offer powerful ways to build wealth. It’s not about which product is universally better—it’s about what fits your investment style.

If you prefer simplicity, SIPs, and guided management, mutual funds may be your go-to.

If you want flexibility, low costs, and control, ETFs might be the better pick.

Both are regulated, diversified, and accessible—so the choice doesn’t have to be stressful. You just need to pick what aligns with your goals, timeline, and comfort with investing tools.

However, always seek professional advice before deciding the best for yourself. Hyperbola is an AMFI-regulated Mutual Fund Distributor, assisting its investors in making risk profile–based decisions.

Sign up on Hyperbola to better assess your risk profile and start investing.