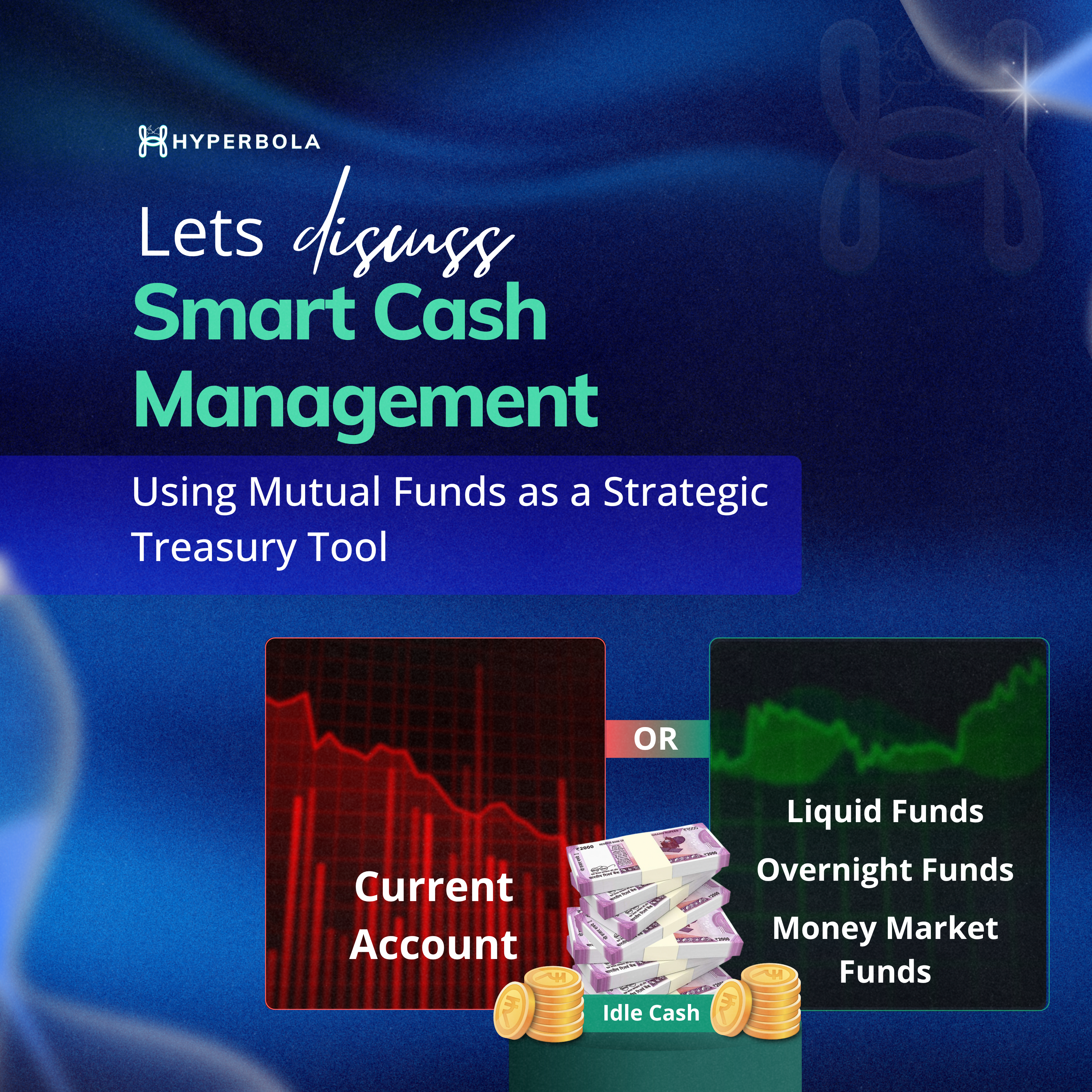

In today’s dynamic financial landscape, the question is no longer whether your surplus funds should work for you—but how quickly and effectively they can. Gone are the days when idle cash would sit in current accounts or be locked up in low-yield fixed deposits.

Today, mutual funds—especially liquid and overnight funds—are emerging as practical, regulation-backed instruments within treasury and cash management services.

Let’s explore how cash management, traditionally a banking domain, is evolving with mutual funds as a viable asset class, and why this shift matters for anyone managing short-term cash needs.

Understanding Cash Management Services: The Foundation

Before diving into mutual funds, it’s important to understand the core of cash management services.

These are a set of tools and processes used to monitor, analyze, and optimize an organization’s cash flow—primarily in the short term.

Put simply, cash management helps ensure that money moves in and out of your system efficiently. It balances liquidity with returns and gives you visibility into how much working capital is available at any given moment.

Banks have historically provided cash management services, handling payments, collections, and liquidity pooling. But as the finance landscape matures, investment options are being layered onto these systems—mutual funds being one of the most agile choices today.

Cash Management meaning in the modern context

When we talk about cash management in today’s terms, we refer not just to handling cash, but to deploying it strategically. It’s about maximizing every rupee of idle money without sacrificing liquidity or risk controls.

This means having:

- Real-time visibility into cash positions

- Automated investment sweeps into short-term instruments

- Safe, same-day access to funds when needed

In this framework, mutual funds offer an appealing intersection of safety, returns, and flexibility—making them a strong contender among asset classes used for daily cash operations.

What is a Cash Management Service?

At its core, a cash management service ensures that you never have too much or too little liquidity. It allows corporations or institutions to automate how excess cash is swept into return-generating avenues.

These services typically include:

- Cash flow forecasting

- Payment and collection solutions

- Investment management for surplus cash

Traditionally provided by banks, these services are increasingly being supplemented by mutual fund offerings, which allow even short-term idle funds to generate meaningful returns.

When mutual funds plug into this system, they become a part of how treasury teams manage working capital—not just invest long-term.

Key Cash Management objectives and how Mutual Funds align

To understand why mutual funds work so well in this space, let’s first break down the objectives of cash management.

The goal is not just to invest—it’s to do it smartly within the tight timelines and risk mandates of business operations.

1. Liquidity

The primary goal of any treasury function is to maintain liquidity. Mutual funds, especially overnight and liquid funds, offer T+0 or T+1 redemption cycles, ensuring money is available when needed without being locked in.

2. Capital Preservation

Cash management is not about aggressive growth—it’s about minimizing loss while maximizing returns. Mutual funds used for treasury, such as liquid or ultra-short duration funds, carry minimal risk due to their focus on high-quality instruments like treasury bills and commercial papers.

3. Yield Optimisation

Idle cash in a current account earns nothing. Even a modest 5–6% annualized return from a liquid mutual fund can significantly improve the financial efficiency of your operations.

4. Automation and Flexibility

Several fund houses offer APIs and CMS integrations that allow automatic sweeps into and out of mutual fund schemes, syncing seamlessly with your treasury management workflows.

This alignment of cash management objectives with the benefits of mutual funds makes them a natural fit for modern treasury operations.

Mutual Funds as a Cash Management Tool: Where they fit

So how do mutual funds become part of a cash management system?

It starts with a shift in mindset—viewing mutual funds not only as long-term investments but also as short-term liquidity tools.

Thanks to regulatory structures, transparent portfolios, and ease of redemption, funds like liquid funds, overnight funds, and money market funds are increasingly being positioned as alternatives to traditional instruments like fixed deposits and sweep accounts.

Mutual funds can be used to:

- Park temporary surplus cash for a few days to a few months

- Earn better yields without locking capital

- Automate investments based on cash balance thresholds

- Build ladders of different fund types for staggered liquidity access

This setup is especially helpful for entities that see frequent fluctuations in receivables and payables and cannot afford the rigidity of term deposits.

Corporate Cash Management: Modern use of Mutual Funds

In the context of corporate cash management, mutual funds offer scalability, control, and returns that align with institutional needs. What used to be a domain for treasury desks at large corporations is now accessible even to medium-sized businesses and institutions.

Some mutual fund companies now offer:

- Dedicated institutional portals for treasury transactions

- Pre-approved limits for redemption

- Customized reporting for audit and compliance teams

This evolution means that corporates can not only manage payments and collections through CMS providers but also integrate mutual funds into their treasury architecture.

In short, mutual funds are no longer just passive investments—they are active treasury tools.

Transitioning from traditional cash tools to Mutual Funds

Making the move from traditional tools like FDs or savings accounts to mutual funds isn’t about disruption—it’s about evolution. You don’t have to overhaul your existing systems; mutual funds can work alongside them.

For example, instead of using a fixed deposit for quarterly tax provisioning, a corporation may opt for a money market fund, which offers similar safety with higher liquidity.

Likewise, instead of idle cash sitting in a zero-yield current account over a weekend, it can be deployed into an overnight fund, earning returns without compromising access.

This step-by-step integration is what makes mutual funds so compelling for modern treasury teams looking for flexibility and performance.

How to use Mutual Funds within your Cash Management Strategy

Once you understand the value, it’s about building the right strategy around mutual funds. Here’s what that could look like:

1. Segment Your Surplus

Break your idle cash into tiers—immediate (1–2 days), near-term (up to 30 days), and medium-term (1–3 months). Match each with the appropriate fund type: overnight, liquid, or ultra-short duration.

2. Work with an MFD or Institutional Partner

Collaborate with a mutual fund distributor who understands risk profiling and cash flow needs. This helps you avoid unsuitable products and ensures regulatory compliance.

3. Automate Sweeps and Reporting

Use APIs or integration services from fund houses that allow daily sweeps, dashboards, and consolidated reporting.

4. Monitor and Rebalance

Set internal benchmarks for acceptable returns and liquidity needs. Review fund performance monthly and rebalance if necessary.

This is not a one-size-fits-all approach. The best mutual fund mix for your treasury depends on your cash cycles, liquidity buffer needs, and risk appetite.

Conclusion

Incorporating mutual funds into your cash management services strategy can create a smarter, more responsive financial engine. Whether you’re managing payments, planning for payroll, or simply avoiding idle capital, mutual funds offer a well-regulated, accessible, and liquid alternative to traditional short-term tools.

You’re not just moving money—you’re optimising it.

And incorporating cash management services into this framework through mutual funds can help create more dynamic, high-performing treasury systems.

However, always seek professional advice before deciding the best strategy for your organisation. Hyperbola is an AMFI-registered Mutual Fund Distributor, assisting investors in making risk profile–based decisions.

Sign up on Hyperbola to manage cash smartly through curated goals and baskets for corporates to invest in.

FAQs

1. What is the meaning of cash management services?

Cash management services refer to the processes and tools used to efficiently handle a company’s cash inflows and outflows. It includes cash flow forecasting, payment solutions, investment of surplus funds, and ensuring liquidity for daily operations.

2. How do mutual funds help in corporate cash management?

Mutual funds—especially overnight and liquid funds—offer safety, liquidity, and yield, making them ideal for parking idle corporate cash. They also allow automation and integration into treasury systems, helping streamline short-term fund deployment.

3. Are mutual funds safe for short-term treasury use?

Yes, especially categories like overnight and liquid funds that invest in high-quality debt instruments. They are regulated by SEBI, offer high liquidity, and have historically low risk compared to long-duration or equity funds.

4. Can mutual funds replace fixed deposits in cash management?

While not a direct replacement, mutual funds can serve a similar role with greater flexibility and potentially better returns. Their low lock-in periods and instant redemption options make them attractive for treasury managers seeking daily or weekly liquidity.